List of leading chip industry chain segments in China.

The article was transferred from WeChat WeChat official account’s "Semiconductor Industry Watch" (ID: ICBank)

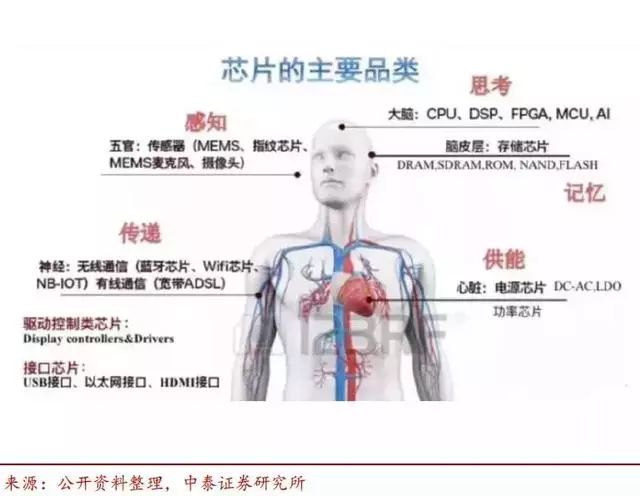

First, let’s take a look.Classification of chips:

Pictures fromWechat WeChat official account "semiconductor industry observation"

In daily life, we can find the types of chips, such as communication chips, artificial intelligence chips, LED chips, computer chips and so on.

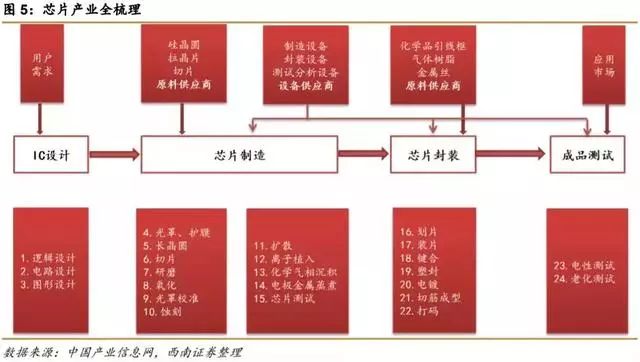

Industrial chain of chipsHere’s the thing:

According to the industrial chain division, the core link of the chip from design to factory mainly includes six parts:

(1) Design softwareChip design software is a key tool for chip companies to design chip structures. At present, the structural design of chips mainly depends on EDA (Electronic Design Automation) software.

(2) instruction set systemFrom a technical point of view, the CPU is only a high collection of millions of small switches, without an efficient instruction set system, the chip can not run the operating system and software;

(3) Chip design, mainly connected to the interface of electronic products and services;

(4) Manufacturing equipment, that is, the equipment for producing chips;

(5) Round crystal OEMThe wafer foundry is the production workshop of chips from drawings to products, which determines the performance indexes such as nano-technology adopted by chips;

(6) Packaging test, which is the last link before the chip is sold, is mainly aimed at ensuring the quality of the product and has relatively low technical requirements.

Overall, inIn most industries such as instruction set and design, the status of China chip industry is very weak.There is a big gap between China and European and American chip industry enterprises. However, in the sectors with relatively low technical requirements, such as wafer foundry, packaging and testing, is expected to take the lead in rising and become a field that is expected to catch up with the world average.

Domestic chip industry chain and main manufacturers;

Image from: Southwest Securities Research Report

What are the leading players in each subdivision of the chip??

The leading memory chip design in China is Zhaoyi innovation;

The domestic GPU leader is Jing Jiawei;

Yangjie technology is the leader of semiconductor discrete devices in China;

SMIC is the leader of wafer foundry in mainland China;

Sanan Optoelectronics is the global leader in LED chips;

Silanwei is a domestic IDM quality enterprise;

North Huachuang is the leader of domestic semiconductor equipment;

Zhichun Technology is the only A-share high-purity process system integration supplier;

Jingrui Co., Ltd. is a leading enterprise in microelectronics chemicals in China;

Zhongke Shuguang is a leading enterprise in high performance computing in China;

Ziguang Guoxin is a listed company in the semiconductor industry under Ziguang Group, and is currently the leading supplier of integrated circuit chip design and system integration solutions in China.

Beijing Jun is the leading enterprise of embedded processor chips;

Zhongying electronics is a domestic high-quality IC design company;

Huiding Technology is a global leader in biometric chips;

Changdian technology is a domestic semiconductor packaging and testing leader;

In addition to the above leading sub-sectors worthy of further study, we can also pay attention to the investment targets of the National Integrated Circuit Industry Fund (referred to as the "Big Fund") in recent years. Please add WeChat WeChat official account: robotinfo Ma Yun is paying attention.

Everbright Securities summarized the investment targets of "big funds". As of January 19, 2018, big funds have become shareholders of more than 50 companies, involving 18 A-share companies and 3 Hong Kong stock companies. At present, the stock market value of big funds exceeds 20 billion yuan.

Here are some good A-share chip companies.

Zhaoyi innovation: domestic storage faucet

As a domestic storage leader, Zhaoyi Innovation ranks among the top three in the global Nor flash market, and with the withdrawal of Japanese and American companies, its market share continues to increase; The storage price keeps rising, and the company’s profitability is bright.

The company builds IDM storage industry chain. In October 2017, the company and Hefei Industrial Investment Holdings (Group) Co., Ltd. signed a cooperation agreement on memory research and development, and jointly carried out the research and development project of 12-inch wafer memory (including DRAM, etc.) with a process of 19nm memory, namely Hefei Changxin. At present, the research and development is progressing smoothly.

Jiangfeng Electronics: Domestic Target Tap

Ultra-high purity metal and sputtering target are one of the key materials in the production of VLSI. The company’s ultra-high purity metal sputtering target products have been applied to the cutting-edge manufacturing technology of world-renowned semiconductor manufacturers, achieving mass supply at the 16-nanometer technology node, successfully breaking the monopoly pattern of multinational companies in the United States and Japan, and also meeting the mass production demand of domestic manufacturers at the 28-nanometer technology node, filling the gap in China’s electronic materials industry.

The company cooperated with Garber in the CMP project in the United States, and won the first order for domestic CMP polishing pads in November 2017.

North Huachuang: the leader of domestic equipment

As the equipment leader, North Huachuang has benefited deeply from the current wave of wafer factory expansion. The company’s business covers integrated circuits, LEDs, photovoltaics and other fields, and many equipments have entered the 14-nanometer process.

The company’s product line covers seven core categories such as etcher, PVD, CVD, oxidation furnace, cleaning machine, diffusion furnace and MFC, and its downstream customers are mainly domestic first-tier fabs such as SMIC, Changjiang Storage and Huali Microelectronics.

Ziguang Guoxin: storage design+FPGA

The company is a leading memory chip design company in China. The layout of the company includes the acquisition of 51% equity of Xi ‘an Huaxin held by Shandong Huaxin, and the total shareholding has increased to 76%, achieving the goal of becoming the first echelon of domestic memory design. At present, the company’s newly developed DDR4 products are being verified and optimized. Recently, the company started to make efforts on FPGA.

Gaode infrared: infrared chip faucet

As the only manufacturer in China who has mastered the second-class superlattice focal plane detector technology, Gaode Infrared has successfully developed engineering products, which means that new breakthroughs have been achieved in blank areas such as photoelectric "anti-missile" and "anti-satellite". At the same time, the popularization and application of mass and low-cost core devices in the civil field has also established the competitive position of infrared chips made in China in the domestic and even international infrared industry.

SSE Information learned that in 2017, the company’s military orders were partially postponed due to the military reform, and the latest news is that the postponed orders will be resumed without affecting the new procurement plan for 2018.

Huatai Securities believes that vertical division of labor has become the development direction of the business model of the semiconductor industry. It is mainly composed of the following three parts: design, manufacture and sealing test. Revenue accounts for about 27%, 51% and 22% of the total sales revenue of the industrial chain respectively.

Chip design company

The top ten in China are Huawei Hisilicon, thunis Zhanrui, ZTE Microelectronics, Huada Semiconductor, Zhixin Microelectronics, Huiding Technology, Silanwei, Datang Semiconductor, Duntai Technology and Zhongxing Microelectronics.

Important companies:

First place: Haisi

There are a lot of HiSilicon processors and HiSilicon baseband chips in the Huawei mobile phones you use, and HiSilicon chips are also available in the smart TV and security system you bought. HiSilicon will be the largest chip design company in China for a long time, and will rise with the growth of Huawei Group in the future. Qualcomm, the world’s number one, earned $15.4 billion in 2016, 3.5 times that of Haisi.

Second place: Ziguang Zhanrui

Spreadtrum, founded after the merger of Rideco, is currently the largest supplier of Samsung mobile phone processors and baseband chips except its own products. The Samsung mobile phones you bought are mainly low-end series, and the chips inside are Ziguang Zhanrui.

Third place: ZTE Microelectronics

Mainly some chips used in our own communication equipment, and mobile phone chips are still purchased.

Fourth place: Huada Semiconductor

China Electronics and Information Industry Group Co., Ltd. (CEC) is a group company formed by integrating its integrated circuit enterprises. It has a large share in smart cards and security chips, smart card applications, analog circuits, new displays and other fields. At present, Huada Semiconductor has three listed companies, including A-share Shanghai Belling and Hong Kong stock company CLP Holdings and Jingmen Technology.

Fifth place: Zhixin Microelectronics

It is a wholly-owned subsidiary of State Grid Information Industry Group, covering three business directions: chip sensing, communication control and energy saving, and is committed to becoming a provider of high-end products, technologies, services and overall solutions with smart chips as the core.

Sixth place: Huiding Technology

Is a listed company, the company has achieved the second place in the field of fingerprint identification chips in the world, second only to AuthenTec, which provides fingerprint identification chips for Apple.

Seventh place: Silan Microelectronics

LED lighting driving IC is one of its main business income, and it also provides variable frequency motor control chips for home appliance enterprises.

Eighth place: Datang Semiconductor

Industrial layout with smart terminal chips, smart security chips and automotive electronic chips as the core.

Ninth place: Duntai Technology

Founded in the United States in 2005, it is committed to the research and development of man-machine interface solutions, providing the most competitive capacitive screen touch chip, TFT LCD display driver chip, touch display integrated single chip (IDC supporting embedded panel), fingerprint identification chip and pressure touch chip for mobile electronic devices.

Tenth place: Zhongxing Microelectronics

Occupy more than 60% of the global market share of computer image input chips. In 2005, Zhongxing Microelectronics was successfully listed on the NASDAQ stock market in the United States. At the beginning of 2016, Zhongxing Microelectronics launched the world’s first SVAC video codec SoC with integrated neural network processor (NPU), which enabled intelligent analysis results to be encoded with video data at the same time to form a structured video stream. This technology is widely used in video surveillance cameras, which opens a new era of intelligent security monitoring.

The key listed companies are: Ziguang Guoxin, Zhaoyi Innovation (Memory), Huiding Technology, Shilanwei (IDM), Datang Telecom, Quanzhi Technology, Zhongying Electronics (household appliances MCU, lithium battery, etc.), Beijing Junzheng, Apex, Fuhanwei, etc.

Chip manufacturing field

Similar to the panel industry, the manufacturing of semiconductor industry is an asset and technology-intensive industry, with large equipment demand, high technology content and high added value. The investment of a single factory is in the order of tens of billions. According to the data, a state-of-the-art 12-inch wafer production line needs to invest about 45 billion yuan, and TSMC’s 3-nanometer factory investment is expected to be 20 billion US dollars. Key listed companies are: SMIC, Hua Hong Semiconductor, etc.

Memory chip field

At present, the three major memory manufacturers in China are in the intensive construction stage. It is expected that they will enter the equipment installation stage in the first half of 2018, and a new round of equipment commissioning and installation drama will be staged soon.

Yangtze river storage:In March 2016, the national memory base with a total investment of about 160 billion yuan was launched in Wuhan. Four months later, Changjiang Storage Group was formally established, and Ziguang Group participated in the second phase of Changjiang Storage. According to Wuhan Xinxin, the registered capital of Changjiang Storage is invested in two phases. The first phase was jointly funded by the National IC Industry Investment Fund, Hubei Guoxin Industry Investment Fund and Hubei Science and Technology Investment Group, the shareholder of Wuhan Xinxin, and the Yangtze River Storage was established on the basis of Wuhan Xinxin IC Manufacturing Co., Ltd. (namely "Wuhan Xinxin"). The second phase will be jointly funded by Ziguang Group and the National Integrated Circuit Industry Investment Fund. Changjiang Storage will take chip manufacturing as a breakthrough, integrating memory product design, technology research and development, wafer production and testing, and sales. It is estimated that the monthly production capacity will be 300,000 pieces by 2020, and the monthly production capacity will be 1 million pieces by 2030.

Jinhua memory integrated circuit production project is located in the integrated circuit industrial park in Jinjiang, Quanzhou. It is jointly invested by Fujian Electronic Information Group and Quanzhou and Jinjiang governments. The total planned area is 594 mu, and the first phase investment is 37 billion yuan. The construction content includes wafer manufacturing and industrial chain support. It is estimated that the production scale of 60,000 12-inch advanced process memory wafers will be formed in September 2018. After the project is completed, it will fill the gap in the mainstream memory field in China. It is reported that as a key DRAM memory production project supported by the state, Jinhua Project has been included in the list of major projects in the national "Thirteenth Five-Year Plan" for major integrated circuit productivity layout planning, and has been supported by the national special construction fund.

Hefei changxinIs a memory project jointly developed by Beijing GigaDevice and Hefei Municipal Government. Invested 7.2 billion US dollars (about NT$ 216.646 billion) to build a 12-inch wafer factory to develop DRAM products. After completion in the future, it is estimated that the maximum monthly production will be as high as 125,000 chips.

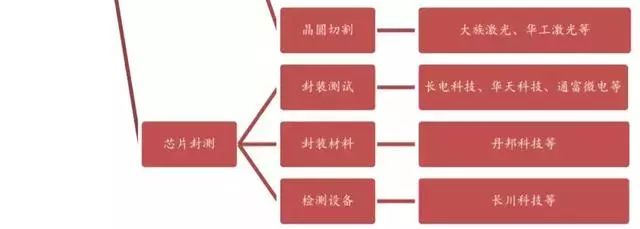

Sealing and testing field

Key listed companies include: Changdian Technology (leading company), Huatian Technology (excellent financial indicators), Tongfu Microelectronics, Taiji Industry (DRAM sealing and testing, clean room), Shenzhen Technology, etc.

Integrated circuit equipment

There are only four wafer manufacturing equipment suppliers above designated size in China, accounting for 7%: according to the report of global wafer manufacturing equipment suppliers above designated size released by Gartner, there are 58 equipment companies in its statistical range, and China only holds 4 seats, namely North Huachuang, Zhongwei Semiconductor, Shengmei Semiconductor and Mattson (acquired by Yizhuang Guotou in 2016), and the others are located in Japan, 13 in the European Union, 10 in the United States, 7 in South Korea.

The key listed companies are: North Huachuang, a leader in high-end IC process equipment, Changchuan Technology, a leader in testing equipment (covering the whole field of manufacturing and packaging), and high-purity process leader to pure technology (lithography, etching, etc.), all of which use chemicals and special gases and have high requirements on purity. Pure technology is to control the purity of gas) and single crystal equipment leader Jingsheng electromechanical, etc.

semiconductor material

China’s semiconductor manufacturing materials industry maintained a sustained growth trend. In 2016, the sales revenue of semiconductor materials enterprises in China was 25.6 billion yuan. It is estimated that China will become the third largest market in the world after 2018. The localization of material supply chain is not only conducive to the control of manufacturing cost, rapid and timely response of service, safe and controllable technology, but also brings more industrial synergy benefits.

The key listed companies are: with the continuous breakthrough of reagent purification and transportation technology, the amount of wet electronic chemicals is relatively certain in a short period of time, and it is suggested to focus on domestic leading Jingrui Co., Ltd. and Jianghuawei; At present, the target material is the first sub-industry of semiconductor core industry chain in China, so it is suggested to focus on Jiangfeng Electronics, the domestic target leader. Large-size silicon wafer is also a relatively certain field in the future. It is suggested to pay attention to Shanghai Xinyang, a pioneer company that is already in the trial production certification stage. In addition, Nanda Optoelectronics in the field of photoresist and Dinglong shares in the field of CMP polishing pad are expected to take the lead in technological breakthroughs and realize import substitution at an early date.